Luke Wedmore and William Sturgeon, research analysts at MS Amlin, review the evidence and impact of supershear earthquakes and discuss how the effects of this type of earthquakes are currently missing from seismic design codes, national seismic hazard models, and catastrophe models used by the (re)insurance industry. With major updates due for earthquake catastrophe models in the next few years, now is the time to act!

Up to 66% of the insured loss from major earthquakes in the past 10 years comes from earthquakes that experienced a phenomenon known as supershear rupture. This should concern the (re)insurance industry as supershear earthquake ruptures are not accounted for in current national seismic hazard models, seismic building codes, or catastrophe models used by the industry. Until the past year or so, few in the (re)insurance industry will have been concerned by the finer details of earthquake rupture physics. With many of the recent most damaging earthquakes being supershear, this blind spot must now be addressed. We discuss how risk carriers and catastrophe model vendors can tackle this gap and illustrate deterministic scenarios and sensitivity tests that can be used to assess supershear risk in the short term.

What are supershear earthquakes?

“An earthquake where the rupture speed is faster than seismic shear (S) waves.”

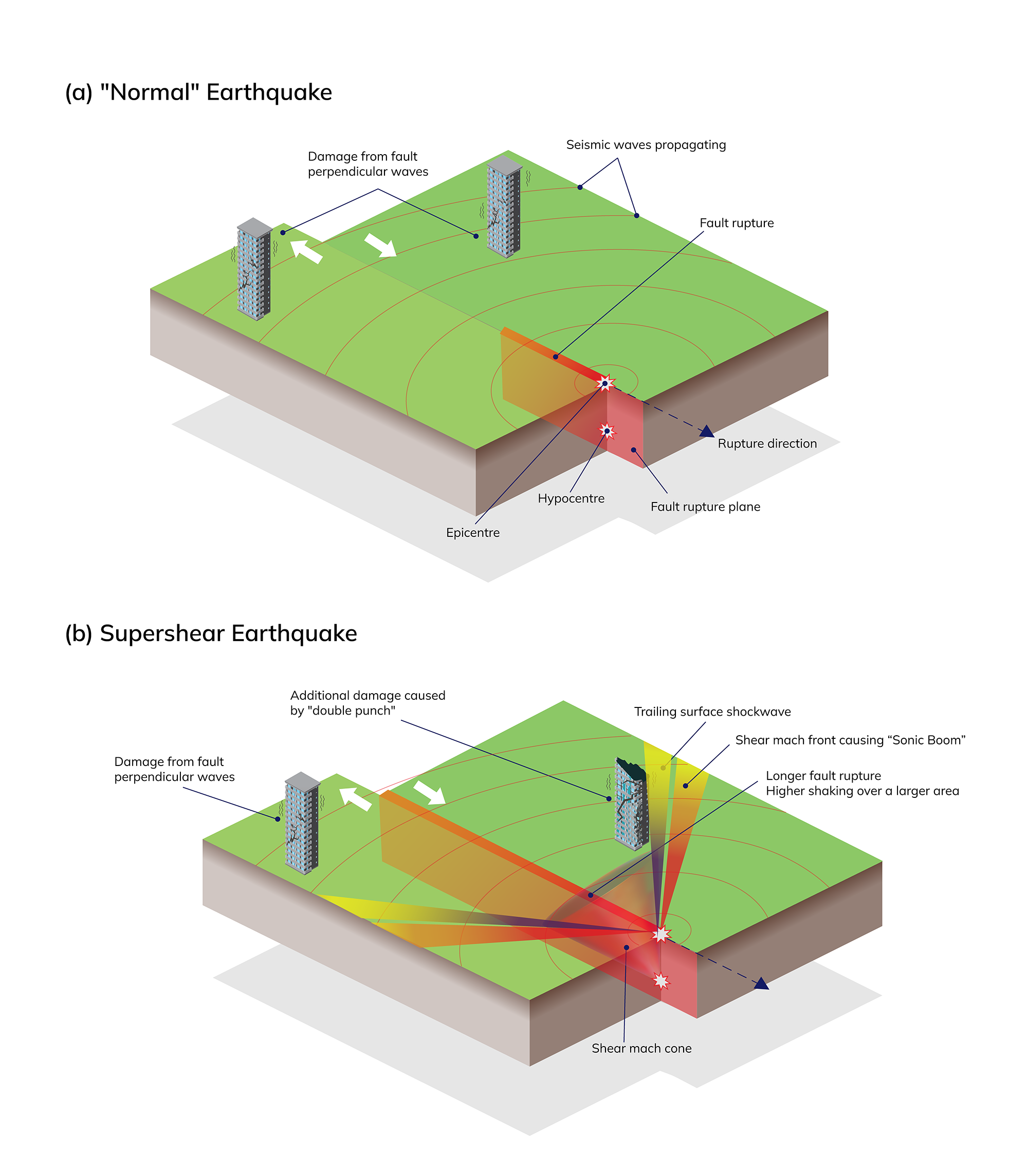

When an earthquake starts, two types of seismic body waves propagate away from the point of rupture (the hypocenter): faster pressure (P) waves and slower shear (S) waves. When these S and P waves reach the surface, they cause surface waves, which normally cause most damage to buildings. The speed at which the earthquake rupture propagates away from the hypocenter is usually the same or slower than the S wave speed (Figure 1a). However, in certain circumstances, earthquake ruptures propagate faster than the S waves, at speeds approaching the P-wave; these earthquakes are known as supershear ruptures (Figure 1b).

Figure 1: The difference between (a) a 'normal' earthquake, where rupture velocity is less than the S wave speed and (b) a supershear earthquake where rupture velocity exceeds the S wave speed.

Supershear ruptures create a shock front, known as a Mach cone, that radiates away from the fault. This shock front is akin to a sonic boom produced when jets exceed the speed of sound. The destructive waves from the shock front are far stronger than seismic body waves generated by normal earthquakes and this stronger level of shaking propagates further away from the fault. Moreover, supershear ruptures deliver a ‘double punch’ of extremely intense shaking: the initial pulse from the supershear shockwave and a second pulse from a trailing surface wave shockwave. This creates unusual torsional loads on buildings, with taller multi-story buildings particularly vulnerable. Although building codes are naturally conservative, these types of loads are not actively considered in current seismic engineering design codes.

The higher rupture speeds that are seen in supershear earthquakes compared with ‘normal’ earthquakes allows supershear earthquakes to propagate further along a fault. This process increases the area that experiences high shaking by the extra rupture length to the power of 2. This effect can be considerable: the 2025 magnitude 7.7 Myanmar earthquake, which was a supershear earthquake, had a surface rupture of 475 km (Goldberg et al., 2025). This is 230 km further than predicted by empirical estimates of fault rupture length (e.g. Leonard, 2010). These ‘ultralong’ ruptures are not considered in current seismic hazard models or catastrophe models.

Fault segments of an earthquake that has experienced supershear rupture often have lower aftershock productivity because of more complete stress reduction across the fault segment that ruptures (Bouchon and Karabulut, 2008). Instead, aftershocks cluster on faults surrounding the earthquake rupture as the shock front induces high stresses in surrounding rock and simultaneously reduces the ability of surrounding faults to store elastic stresses. Consequently, supershear ruptures are thought to raise the likelihood of earthquake doublets and/or clustered sequences, where a second (or subsequent) major earthquake occurs on a surrounding fault (Dunham and Bhat, 2008). The corollary of this is that if a supershear earthquake almost totally relieves stress on a ruptured fault, there is likely to be longer repeat times between large earthquakes on supershear capable fault segments. Following the supershear 1906 San Francisco earthquake, the largest aftershocks were observed at the ends of the rupture, with few events along the main earthquake rupture. In addition, The San Andreas Fault, the causative fault of the 1906 earthquake, has been absent of major or moderate earthquakes in the years since 1906.

In summary, supershear earthquakes can cause substantially higher levels of damage compared with a ‘normal’ earthquake rupture because:

- supershear ruptures generate a Mach cone, a zone of intense shear shockwaves that cause elevated levels of shaking.

- buildings are affected by a ‘double punch’ of seismic waves that causes high torsional loads, particularly in multi-storey buildings.

- supershear ruptures are often longer than sub shear ruptures, with the increased area undergoing damaging shaking scaled by the longer rupture length to the power of 2.

- There is potentially an increased likelihood of earthquake doublets or an earthquake sequence.

How common are supershear earthquakes and where do they occur?

‘Supershear earthquakes account for approximately one third of large strike slip earthquakes and occur on strike slip faults (e.g. San Andreas, North Anatolian faults)’

Supershear earthquakes were thought to be rare when they were first observed in the early 2000’s. Since 2010, the number of supershear earthquakes observed has increased as levels of seismic instrumentation around the world have improved. It is now estimated that 36% of large (magnitude > 7.0) strike slip earthquakes over the past 15 years have involved supershear rupture (Elbanna et al., 2025).

Supershear earthquakes are confined to strike slip faults, the types of faults that occur at conservative plate boundaries, where portions of the Earth’s crust slide horizontally past each other. In the past 10 years alone supershear earthquakes have been observed in Myanmar in 2025, offshore Cape Mendocino (California) in 2024, Turkey in 2023, the Caribbean Sea in 2020 and 2018, Indonesia (Palu) in 2018, The Aleutian Islands in 2017, and the mid Atlantic ridge in 2016. There are thought to be certain geological conditions that make a fault more susceptible to supershear ruptures, such as a smooth, straight fault geometry, a long period of stress accumulation, and contrasting rock properties either side of a fault, but this remains an area of active research.

Why should the (re)insurance industry care?

‘Supershear earthquakes have occurred on major faults in California and supershear ruptures caused the majority of insured losses from earthquakes in the past ten years.’

California is the world’s largest earthquake (re)insurance market and lies along the conservative boundary between the North America and Pacific tectonic plates. Since the early 2000’s there has not been a supershear earthquake in California (although the 2024 earthquake offshore Cape Mendocino that caused shaking in California was a supershear event; Pollitz et al., 2025). Nonetheless, two notable supershear earthquakes in California have been retrospectively identified: the 1906 magnitude 7.9 San Francisco Earthquake and the magnitude 6.5 Imperial Valley earthquake in 1979. Furthermore, many of the geological conditions thought to be required for supershear earthquakes are present along the major strike-slip faults in California. Thus, given the higher shaking intensities, increased chance of earthquake clusters, and the extra damage likely caused by supershear earthquakes, there is a significant chance that earthquake risk in California is markedly underestimated.

Recent supershear earthquakes highlight the potential increase in damage and insured loss from supershear earthquakes. The Turkey and Syria earthquakes in 2023 saw some of the largest values of peak ground acceleration and velocity ever recorded alongside extremely high spectral acceleration values, which exceeded Turkish design codes (Elbanna et al., 2023). MS Amlin’s analysis of the last 10 years of global insured earthquake losses indicates that supershear earthquakes are responsible for up to 66% of insured loss from major earthquakes (events where insured loss is ≥ USD 1 billion; Table 1). This highlights the current blind spot to supershear earthquakes within the (re)insurance industry, which are not considered in any current catastrophe models.

| Earthquake | Fatalities | Economic Loss (billion USD) | Insured Loss (billion USD) | Supershear? |

|---|---|---|---|---|

| Myanmar, 2025 | 5,456 | 16 | 2 | Yes |

| Noto, Japan, 2024 | 489 | 18 | 1 | No |

| Turkey & Syria, 2023 | 59,272 | 92 | 5.7 | Yes |

| Fukushima, Japan 2022 | 3 | 9 | 2.8 | No |

| Fukushima, Japan 2021 | 1 | 8 | 2.5 | No |

| Mexico 19/09/2017 | 370 | 5 | 1 | No |

| Kumamoto, Japan 2016 | 154 | 38 | 5.5 | Uncertain |

| Kaikoura, New Zealand, 2016 | 2 | 4 | 2.1 | No |

What are the implications for earthquake catastrophe models?

‘Supershear earthquakes mean that the tail of earthquake catastrophe models might be underestimating loss at return periods used for capital and solvency decisions.’

The two major catastrophe model vendors within the (re)insurance industry – Verisk and Moody’s – are updating their U.S. earthquake models following the 2023 update to the U.S. national seismic hazard model. At the same time, California is experiencing its longest earthquake (magnitude > 6.5) drought in the past 1,000 years on major faults, which could experience supershear earthquakes (Biasi and Scharer, 2019). Given these factors, future earthquake catastrophe models must urgently incorporate supershear ruptures and their consequences.

It is a considerable task for the catastrophe model vendors to include supershear effects in their next generation of U.S. earthquake models: state-of-the-art supershear earthquakes models are computationally expensive, and normally set up for single rupture scenarios. Consequently, these models require considerable time on high performance computing (HPC) facilities (e.g. Dunham et al., 2011), which may not be available to catastrophe model vendors. Other computational or empirical approaches offer viable alternatives to costly HPC models, despite the lack of near-fault observations of ground shaking caused by supershear earthquakes to constrain ground motion models. Seismic hazard analysis has a long history of using (often loosely constrained) empirical relationships to derive important model parameters, from ground motion prediction equations through to relationships between fault length and earthquake properties. The recent global compilations of the frequency of supershear earthquakes, as well as comparisons between shaking of supershear and non-supershear ruptures, offer clues that can be used to assess the impact of supershear ruptures (e.g. Elbanna et al., 2025; Bao et al., 2022). However, supershear earthquakes cause strong spatial variability in shaking – with areas in the Mach cones experiencing significantly more shaking, with greater variability in shaking direction. These directivity effects are extremely challenging to include unless seismic hazard models move away from their current empirically based approach towards a more physics-based approach.

In the short term, both catastrophe model vendors and (re)insurers can address this gap using deterministic scenarios and sensitivity tests. For (re) insurers, deterministic scenarios are one tool that can be used to identify exposure to supershear earthquakes. To perform these scenario tests, risk carriers require catastrophe model vendors to: i) highlight long strike-slip faults that have the potential for supershear rupture (especially in high materiality regions); ii) develop deterministic sensitivity scenarios with enhanced ground shaking; and/or iii) test directivity scenarios with alternative along-strike shaking patterns, for example elongated or concentrated zones of elevated ground motion in the rupture direction.

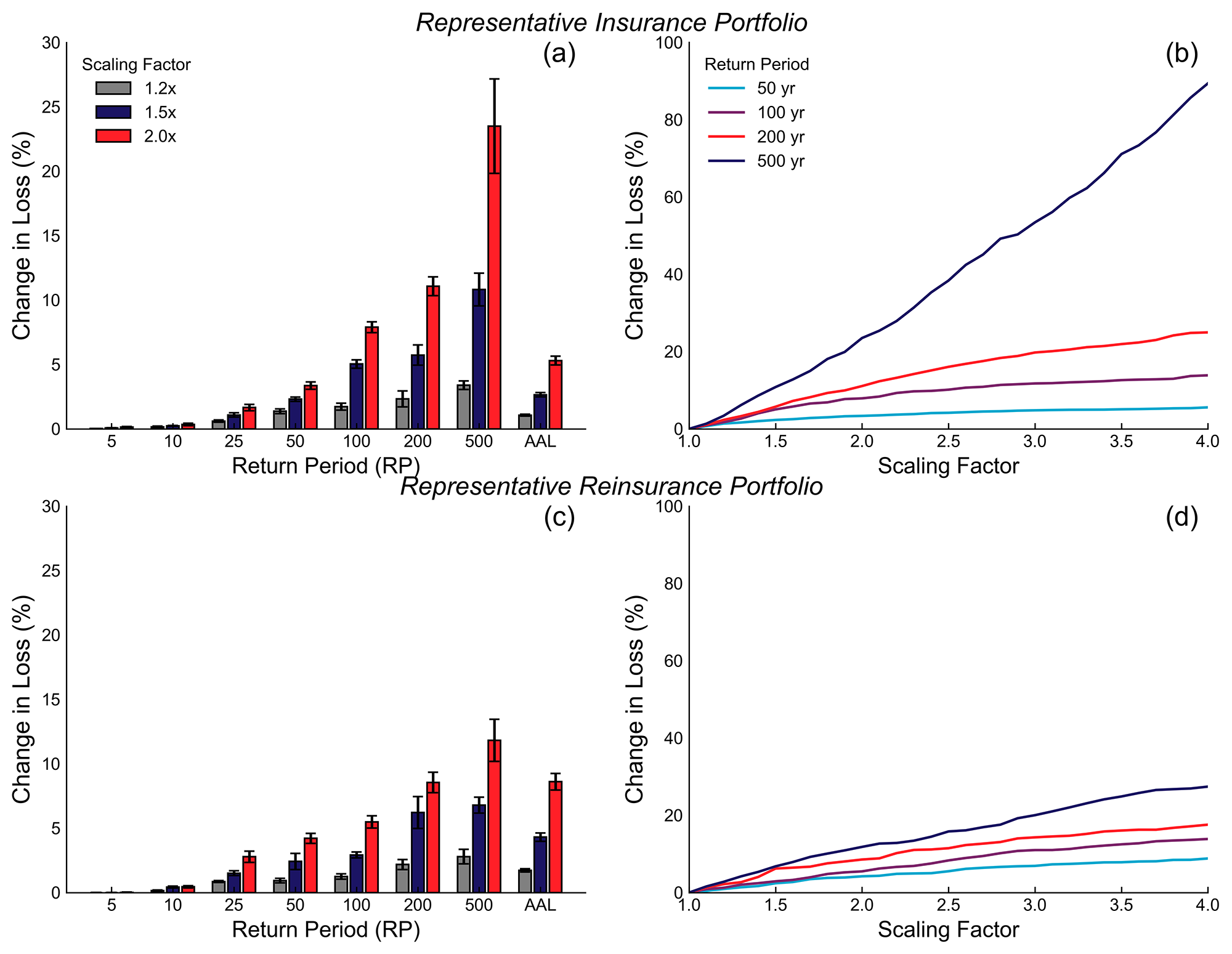

Here we describe a simple illustrative sensitivity analysis that MS Amlin is using to assess the potential impact of supershear earthquakes on catastrophe model outputs that they use for pricing and capital decisions for earthquake risks. This method uses a range of scaling factors to account for increased shaking intensity, shaking area, and ultimately losses from supershear rupture. We randomly selected 36% of magnitude 7.5+ strike slip earthquakes in California and applied a range of scaling factors to these events that mimic the increase in loss that might be expected for a hypothetical supershear earthquake, relative to a normal earthquake. We then re-calculated an exceedance probability (EP) curve for the whole of the U.S. and computed the percentage difference between the unscaled and scaled EP curves. We repeated this analysis multiple times to sample and scale a representative range of supershear events and used representative insurance and reinsurance exposures to test the impacts on different types of (re)insurance portfolios.

Figure 2: Change in loss because of supershear earthquakes. Left hand plots: change in loss at different return periods for three loss scaling factors. Right hand plots: change in loss at different return periods with change in scaling factor. (a-b) representative Insurance portfolio; (c-d) representative reinsurance portfolio.

For the representative insurance portfolio, applying supershear scaling factors causes a <5% change in loss at return periods <100 years, irrespective of the factor used (Figure 1a). The change in the average annual loss (AAL) of the insurance portfolio is similarly ≲5%, irrespective of scaling factor. At higher return periods (>100 years), larger changes in the losses are seen, with the 200-year return period loss for the insurance portfolio increasing by approximately 5% to 10%, depending on the factor used (Figure 1a). Higher return periods are more sensitive to the scaling factor (Figure 1b), with the 200-year return period loss increasing by ~10% with each doubling of the scaling factor, whereas the 500-year return period loss increases by 30%-60% with each doubling of the scaling factor.

The results for the representative reinsurance portfolio differ from the insurance portfolio: the reinsurance AAL change is larger compared with the insurance portfolio (Figure 1c). Similarly, the change in loss for the reinsurance portfolio is restricted to ≲10% for all but the highest return periods and the highest scaling factors (Figure 1c-d). This difference is likely due to a reinsurance portfolio having limits that are more easily exhausted than the total limit within an insurance portfolio. Insurance portfolios sample more lower return periods, where overall loss is lower. Consequently, there is less of an impact on the AAL as the factors are only applied to the larger earthquakes that affect the tail of the loss distribution. In contrast, reinsurance portfolios sample fewer losses at low overall (i.e. pre-reinsurance terms) return periods. Consequently, the AAL increases more as the losses that are sampled are directly affected by the scaling factors.

Given the current empirical evidence for the proportion of strike slip earthquakes that are supershear, this analysis indicates that constraining the change in damage for a supershear vs non-supershear earthquake is important to accurately determine the impact on a (re)insurers portfolio. This is a key area where there is still considerable scientific uncertainty. Given that the potential impact is most sensitive to return periods where capital decisions (both requirements and allocation) are made by (re)insurance companies (e.g. 200-year return period; Kouwenberg, 2017), a prudent approach to capital decisions should account for supershear earthquakes.

Summary

Over the past 15 years there has been a gradual transition from acceptance of the theory predicting the possibility of supershear earthquakes to widespread observations of these earthquakes. The next steps need to involve collaboration between scientists, engineers, risk practitioners and the (re)insurance industry to advance the science and produce practical solutions, regulations and guidance. For the (re)insurance industry, this should focus around: i) raising awareness of supershear earthquakes; ii) improving quantification of the effects of supershear earthquakes within the tail of earthquake catastrophe models; and iii) ensuring that supershear earthquakes are considered when making capital and pricing decisions.

Acknowledgements

The authors thank Samuel Phibbs for his comments on this article and Jane Sedgeman for her assistance in creating Figure 1.

Supershear Earthquakes – An Insurance Blind Spot

Volume 04, article 04

June 4, 2026

Author(s): Luke Wedmore and William Sturgeon

Tags: Comments

DOI: 10.63024/yexc-027r